Equal Housing Lender

Freddie Mac: Lump Sum Repayment is Not Required in Forbearance

Contributors • April 27, 2020

Freddie Mac reiterates repayment policies in the wake of COVID-19

MCLEAN, Va., April 27, 2020 (GLOBE NEWSWIRE) -- Freddie Mac (OTCQB: FMCC) today reiterated that borrowers in forbearance living in homes owned by the company have many options to repay missed payments and are never required to choose doing so in one lump sum.

Freddie Mac CEO David Brickman made the following statement:

“Simply put, if you are a homeowner seeking forbearance and Freddie Mac owns your loan, you are never required to make up missed payments in a lump sum. Our policies offer a number of options to bring borrowers current, including repayment plans, resuming normal payments or lowering your monthly payment through a modification. We encourage homeowners facing hardship to work with their servicer to identify the plan that’s appropriate for their unique situation.”

In March, Freddie Mac announced it was taking a number of actions to assist homeowners facing financial hardship due to COVID-19. These include forbearance, during which a borrower’s payments are reduced or suspended. While borrowers in forbearance must repay the missed payments, full repayment immediately following forbearance is just one of many options, and they are never required to do so.

Owners facing a hardship are entitled to up to 12 months of forbearance. Servicers will start with a shorter plan and reassess to see if an extension for up to 12 months is necessary. Once the hardship has been resolved, there are several options for borrowers to repay the money owed, including:

- Full repayment , known as reinstatement, where you pay back the missed payments and quickly get back on track.

- A repayment plan , which allows borrowers to catch up gradually in addition to paying regular monthly payments.

- Payment Deferral or modification of the loan, to keep monthly payments consistent and add the borrower’s missed payments to the end of the mortgage.

- Modification of the loan , to reduce a borrower’s original monthly payment amount.

Loan servicers will reach out about 30 days before the initial forbearance plan is scheduled to end to determine which assistance program is best or if additional forbearance is needed. Borrowers who believe they are not being offered proper repayment options can reach out to the Consumer Financial Protection Bureau.

Consumers looking for additional resources can visit MyHome® by Freddie Mac.

Freddie Mac makes home possible for millions of families and individuals by providing mortgage capital to lenders. Since our creation by Congress in 1970, we’ve made housing more accessible and affordable for homebuyers and renters in communities nationwide. We are building a better housing finance system for homebuyers, renters, lenders, and taxpayers. Learn more at FreddieMac.com, Twitter @ FreddieMac, and Freddie Mac’s blog FreddieMac.com/blog.

CONTACT: Chad Wandler 703-903-2446 Chad_Wandler@FreddieMac.com

the number of down-payment assistance programs is on the rise, and a growing share are open to people of all income levels — even six-figure earners.

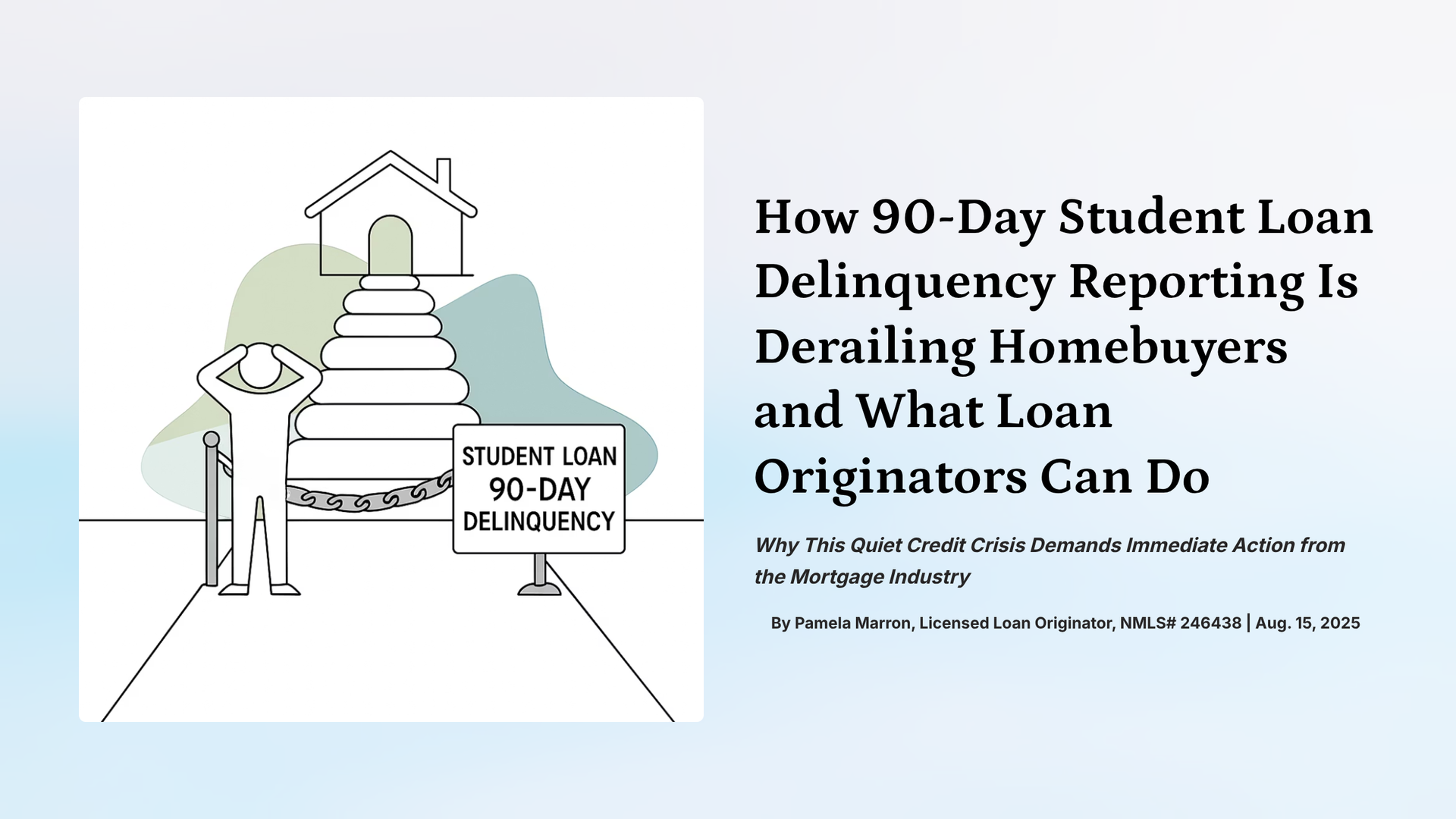

90-day student loan delinquencies are silently crushing credit scores and killing mortgage approvals. Here’s how MLOs can fight back.

A Few Extra Points MLOs Need to Know For Clients With Student Loans