Equal Housing Lender

DIY Down Payment Assistance for MLO's

"Simplify DPAs: Modernizing Access to Down Payment Programs"

Prepared by Pam Marron, Innovative Mortgage Loan Originator, NMLS#246438

with Sean Moss, Vice Pres., Downpaymentresource.com, Down Payment Connect

Simplify DPAs: Modernizing Access to Down Payment Programs

Webinar for Innovative Mortgage Services, Inc. MLOs explains best DPA tools like Downpaymentresource.com, Down Payment Connect, and other information further down on this page to get MLOs and realtors started with DPA.

Home prices are so high that more than half of down-payment assistance programs are now open to buyers earning over $100K

The number of down-payment assistance programs is on the rise as housing costs remain high.

There’s been an increase in the number of down-payment assistance programs across the country. Many now allow prospective buyers who earn over $100,000 to get funding.

Key Points

- The number of down-payment assistance programs increased by 6% over the last year, totaling approximately 2,600 nationwide.

- Sixty-two percent of down-payment assistance programs now support buyers earning over $100,000, with 10% having no income limits.

- The average funding from down-payment assistance programs was $18,000, with over half offering forgivable loans.

Guest Speakers

Below is a representation of different types of Down Payment Assistance programs available for both licensed mortgage brokers and for some retail lending institutions. More DPA programs are available but these descriptions were meant to help MLOs understand the variety of DPA programs out there.

Pamela Marron, Licensed Loan Originator, NMLS# 246438; Innovative Mortgage Services, Inc., NMLS# 250769

1. 1st mortgage lenders that allows 2nd mortgage to be added.

Why are Community 2nds the best?

- Allows client to get the best 1st mortg. rate based off of their credit score.

- Provide most amount of funds available of all DPA and can be used to buydown rate, the loan amount and reduce LTV to alleviate/reduce PMI on conv loans.

- Many will allow re-subordination of 2nd mtg if client needs to refi in future.

- Many allow stacking of more than 1 DPA.

IMPORTANT: Use BOTH mortgage qualifying AND 2nd mortgage calculation to determine amount of DPA client is eligible for!

1st mortgage criteria: Qualify clients with FHA, Conv, USDA guidelines.

- May allow Stacking of additional DPA or grants on top of the 1st mtg. and 2nd mtg.

- FHA, VA, Conv, USDA 1st mortgages allowed.

- Allows seller contribution

- Allows Borrower Paid and Lender Paid

- May allow repair escrow holdback for bank owned property.

2nd mtg. criteria: HUD income level and is based on household income size.

- Often the highest DPA dollar amount available. Can be used towards lowering loan amount, buying out conventional mortg. insurance, buying down interest rate and covering closing costs.

- FTHB requirement commonly.

- Either minimum credit score or allow lower score if AUS approval.

- May have max. front and back DTI ratios unless they allow higher with AUS approval.

- Some have maximum borrower assets allowed.

- Usually deferred for 5 yrs or life of loan, payment not included in DTI.

- May have forgivable option.

- May allow re-subordination of 1st mortgage to allow the client to refinance and keep the 2nd mortgage in place.

- May cap MLO maximum costs.

- Allow seller contribution.

Lenders we can use:

- UWM

- FBC

- Kind Lending

- PennyMac

- Michigan Mutual

- Plaza Home Loans

- PRMG

- Cardinal

- Orion

2. Fl Hometown Heroes/Fl Bond combined 1st and 2nd mtg.

Why is Fl HTH and Fl Bond program the 2nd best?

- One good interest rate for all qualified borrowers no matter what their credit score.

- Qualifying income max. is higher than city and county programs.

- Often Lender Paid points with no point cost to the client.

- Allow stacking of more than one DPA.

- Underwritten and closed by same lender.

IMPORTANT: Use BOTH mortgage qualifying AND 2nd mortgage calculation to determine amount of DPA client is eligible for!

Criteria:

- HUD income level and is based on household income size.

- Some Fl Bond prog’s require tax returns.

- Minimum 640 credit score.

- Pay a maximum Lender Pd comp to MLO.

- Max. DTI ratio.

- Lower interest rate and one rate per program no matter what client credit score is as long as minimum score met.

- HTH covers 5% of sales price and Fl Bonds cover min./max. $10,000 towards DPA and closing costs.

- FHA, VA, Conv., USDA loans available.

- If refinance, must pay off 1st and 2nd mtg.

- Payment deferred for 30 yrs. or property sold and paid off.

- Cap on Processing Fee, commonly.

- Allow seller contribution.

Lenders we can use:

- FBC

- Windsor

- UWM

3. Proprietary wholesaler combined 1st and 2nd DPA mtg. (incl. grants)

Criteria:

- Underwritten/closed by same lender.

- Only FHA loans.

- No income limit.

- No FTHB requirement.

- Use mortgage qualifying ONLY, not 2nd calculation to determine amount of DPA client is eligible for!

- Min. credit score as low as 600 with AUS approval.

- Some are forgivable.

- Some may not have deferred payment.

- Often 3.5% or 5% DPA amount.

- Interest rates are higher.

- Both Borrower and Lender Paid pricing.

Lenders we can use:

- Kind Lending

- Michigan Mutual

- Plaza Home Loans

- Orion Lending

- E-Lend (3.5% FHA grant)

4. Other: 2nds, grants, unique benefit DPA

Go to program for income criteria.

- May require DPA 2nd payment to be included in DTI.

- Commonly use mortgage qualifying ONLY, not 2nd calculation to determine amount of DPA client is eligible for!

- Renovation/repair

- multi-family

- Grants

- Indian Tribes

- Specific business DPA

- Stacking a proprietary DPA with unique benefits with a city/county 2nd mtg. DPA program

Programs we can use:

- Solita's House DPA and Renovation DPA with conventional loans

- Orion Lending: stack proprietary DPA with city/county 2nd mtg.

MLO'S: IMPORTANT NOTICE!

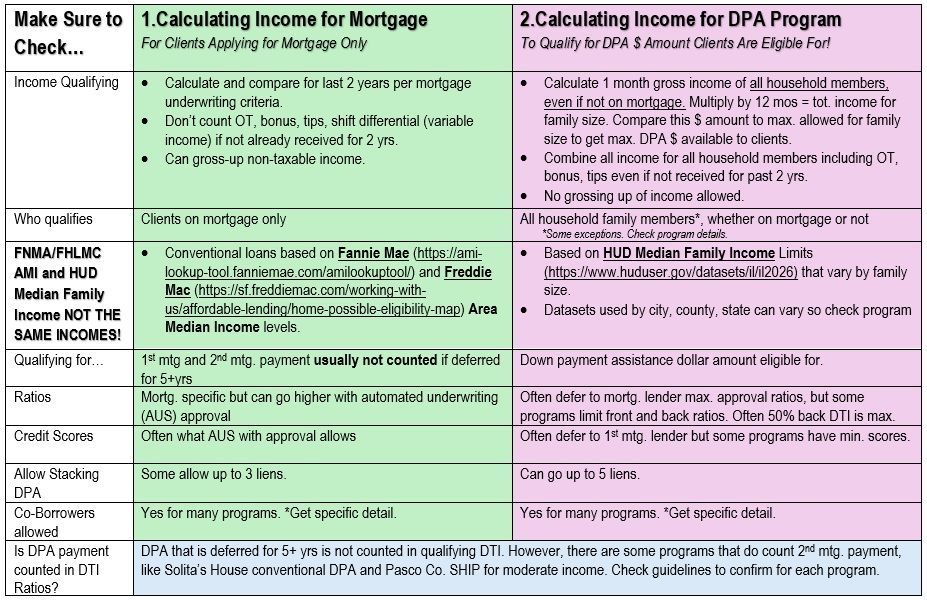

When using city, county SHIP, state and federal down payment assistance, make sure to check and know the following 2 calculations upfront!

1. Calculate income for the mortgage for clients applying for the mortgage only.

2. Calculate income for the DPA program to qualify for the DPA $ amount clients are eligible for.

The income for the eligible DPA amount may be higher than the mortgage qualifying income. This can result in your client being eligible for a lower DPA dollar amount than you think… and that filters down to higher ratios if the DPA dollar amount is decreased. Do this exercise upfront to avoid issues later!

Check With Programs on This FIRST!

- A few DPA programs require that the client be approved through their program upfront before they sign a contract.

- Some DPA programs require the loan originator and realtor to be approved to provide the program.

How DPA Funds Available Can Vary

- Some DPA programs provide funds with varying assistance amounts based upon varying AMI income. And maximum income can also vary by family size.

- Other DPA programs have a maximum income and a maximum dollar assistance available to provide funding between the sales price and the amount of a mortgage to make the home affordable. This type of funding is often referred to as GAP Funding.

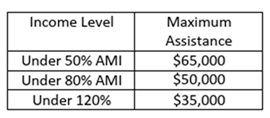

Below is an example of varying DPA $ amount (Maximum Assistance) matched to the Area Median Income Maximum per family size.

Example is for Pasco County SHIP Down Payment Assistance.

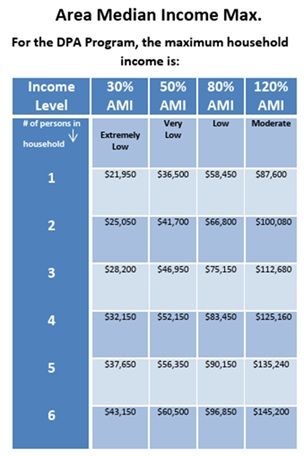

- Max. HUD DPA $ Assistance per AMI (Area Median Income) levels.

- Max. HOUSEHOLD INCOME for all household members age 18 and up, even if not on mortgage. Children who will occupy home are counted. Below is example using Pasco County SHIP Down Payment Assistance.

For all household members over 18 yrs old: average the total gross of paychecks for the last 30 days for borrowers and any household members 18 yrs or older. Do not gross up non-taxable income. Multiply this amount by 12 months to equal yearly income.

Compare this yearly income to HUD AMI% the borrowers must be UNDER for their family size. (on right).

Then check the $amt of funds available for that AMI%. (See above.) This will provide the best estimate of what the borrower should receive for DPA assistance.

Most programs don't require credit of household members not on mortgage to be verified. Check program underwriting guidelines.

Example: a 32 yr old borrowers income for herself and 3 children ages 6,8 and 9 is $68,450. For this family of 4, this income exceeds the 50% AMI of $52,150 but is under the 80% AMI of $83,450, so the borrower is evaluated at 80% AMI.

Per the far left Maximum Assistance for Under 80% AMI, the borrower is eligible for $50,000 down payment assistance.

Income Calculating for DPA Dollars

- Calculate total household income of all household members over age 18 by average 1 month of income (some programs require 2 month average) x 12 months = yearly household income.

- Use ALL gross income including base, overtime, commission, tip income, shift differential even when not received for past two years.

- Calculate CURRENT total income and project forward.

A word about Variable Income...

A growing number of prospective borrowers have Variable Income where hours fluctuate and are not full-time. Often, overtime, shift differential and bonuses are given. This type of income needs to be averaged and should be increasing. It must generally be received for at least 2 years on conventional loans and can be considered for 12 months on an FHA loan.

MGIC* and Essent (Excel) PMI have Variable Income calculators. Also, UWM has a Variable Income calculator that can be used with W-2s and/or paystubs.

*for MGIC: https://www.mgic.com/underwriting/seb#form, signup and use open Employment and other income calculator: Download macro-free. Picture on right.

How to Quickly Evaluate Best DPA Options for Clients

Clients can be funneled to the best DPA for their circumstances using these steps!

If you find that client income is too high for a community 2nd mortgage which has the most conservative income levels, in Florida, Hometown Heroes and then the Fl Bond with higher income levels should be considered. If that income is still too low for clients income, proprietary wholesale DPA should be considered as these programs don't have an income cap.

Steps below are generic and broad with the intent to "funnel down" to the best DPA programs for your client.

Pull Tri-merged credit first. Most DPA programs have a minimum credit score.

Credit Score Simulation & Improvement

If your client needs to fix a few things on their credit first, CreditXpert analyzes credit data and simulates different actions—like paying down balances or removing inaccuracies—to show how those changes could impact the borrower’s credit score.

CreditXpert can show how scores change after:

- balance is reduced to lower utilization.

- problem account is deleted or paid down.

- disputes are removed.

- # of months goes by.

- an account is added or removed.

CreditXpert is available to MLO’s either through a subscription, your credit reporting agency and also available with UWM through Boost.

- Determine mid-score for borrowers.

- If client has student loans and payment is not shown on credit report, have them get payment letter from servicer.

Analyze 2 Income Calc's (shown above) for 1st mtg DTI & Community 2nd DPA

Check into best option of using city, county municipal DPA as a 2nd mtg. that can be added to many FHA, Conv, VA and USDA 1st mortgages.

For 1st Mortgage:

- Retrieve last 2 yrs of year end paystubs and year-to-date paystubs.

- Get employer contact info. for who can verify income for each borrower for Verif. of Employment (VOE). Send out VOE upfront for mortgage clients.

- Qualify borrowers per normal mortgage qualifying guidelines.

For city, county SHIP, state Hometown Heroes and *Fl Bond

- Retrieve 1 month of paystubs (some programs require 2 mos.) for all household members above 18. Multiply monthly gross avg. by 12 months to get qualifiable AMI% income.

- Compare this sum to the DPA program maximum income for your client's total # of household members. Then, retrieve down payment $ amount your clients may receive per their AMI max. level.

*Some Exceptions may apply.

Use DownpaymentResource.com

for FREE to see an overview of what DPA clients are eligible for!

You and your client can go to www.downpaymentresource.com and click on green "Find Down Payment Help" to find what is available for clients. A location is required and a list of DPA options is provided for FREE!

- Provides a basic overview of programs (other than wholesale that client is eligible for.

- FREE public facing website.

- Provides DPA in all 50 states.

MLOs & Realtors: use Down Payment Connect, the BEST DPA tool on the market!

Down Payment Connect, a subscription based program of Downpaymentresource.com, offers MLOs and realtors detailed information about all DPA in your state!

- Comprehensive information on each DPA with contact info., links to flyers, underwriting guidelines, and a great deal of information not often on DPA websites!

- ALL DPA in your state and a growing number of wholesaler programs.

- Incredible filters for what MLOs need to find for clients!

- FREE to many MLS platforms across the U.S. for realtors & creates opportunity to partner MLOs!

- Your own unique landing page to attract DPA seekers to you!

- A front page Directory that shows what type of DPA, max. $ amt and sales price max., if funds are available at-a-glance.

- Ability to keep notes on each program for future reference.

- Notes If community 2nd mtgs will allow re-subordination for future refinance! Not all programs allow this. Noted in Benefits under Program Overview.

- Provides program contacts, Lender Manual, flyers, website, submission portal.

- Provides allowable Homebuyer Ed class options.

- shows which programs allow wholesale, correspondent, retail.

To Be Aware of Upfront...

- Some programs like HTH and Fl Bond have capped 3rd party processing fee which may be lower than your processor normally gets. Be prepared to make up the difference.

- Community 2nds are a totally seperate submission and processors commonly charge for this, approx. $275.

- IMPORTANT: City, county and state DPA use different HUD AMI that has different income levels than Fannie Mae and Freddie Mac, and is based on total income of household members.

- IMPORTANT: Confirm the income calculation method that determines the amount of DPA a client may be eligible for. Most city and county SHIP programs provide different DPA amounts for different AMI incomes but some provide a maximum dollar amount if clients are under a specific AMI%.

Questions below can normally be found on the DPC Program Overview under Application Requirement. If you aren't using DPC, check with DPA provider.

- Does the MLO, realtor need to take a class to get approved BEFORE client can sign a contract?

- Does the client need to get approved UPFRONT with the DPA provider?

- When can a 1st mtg. file be submitted?

- What timeframe is needed by DPA provider to process file and to close?

- Does the provider have a maximum cost the lender/MLO can charge?

- Does the client need to live in or work in city/county DPA is needed for? If yes, what is min. time needed?

Stacking DPA

Yes, you can add a 3rd DPA on top of a 1st and 2nd mtg. in some instances!

- DPC Program Directory for each DPA notes if this is allowed under Benefits and Program Terms.

- For your 1st stacking of DPA, make sure that you as the MLO review the underwriting details (you are considering details now for 3 or more programs!) and follow with processor, title co. and DPA provider!

- They key is to stack a community 2nd on a 2st mortgage or first and 2nd mtg that allows stacking (ie.Hometown Heroes or Fl Bond as 1st and 2nd and then add 2nd mtg. in 3rd place.)

Repair Escrow

Some 1st mortgage lenders will allow DPA for repairs to be used.

- Commonly, only repairs noted on appraisal can be repaired.

- This is normally allowed when the property is bank-owned or repairs are necessary for safety reasons.

- A cost of 120-150% of the repair invoice is commonly held back by the title company until the repairs are done. After a final inspection to insure all work is completed, the asdditional escrow cost not used can be refunded.

- The seller or the buyer can proivde the cost for the escrow holdback.

Resources

Florida 2025 Hometown Heroes Bond and TBA Guidelines and more!

pardon us while we populate resources!

This is paragraph text. Click it or hit the Manage Text button to change the font, color, size, format, and more. To set up site-wide paragraph and title styles, go to Site Theme.

DPA Articles to Help MLOs

the number of down-payment assistance programs is on the rise, and a growing share are open to people of all income levels — even six-figure earners.

Streamlining the Path to Homeownership: The Benefits of Using HomePrep to get Clients Mortgage-Ready

Learn how Mortgage Loan Originators (MLOs) can assist clients in overcoming credit, budgeting, and down payment challenges through HomePrep.

Down Payment Connect is already being used by MLOs and Realtors. Now it's available to HUD Counselors through HomePrep! Down payment assistance is quickly rising to the top need for clients wishing to purchase a home. Down Payment Connect , the back-end data provider for the parent Downpaymentresource.com , houses every down payment assistance program in the US and provides extremely detailed information laid out in a consistent format for each DPA program in their system. Throughout the last two years, Downpaymentresource.com administrators have worked with MLO’s and the HomePrep developers to add nearly all wholesale down payment assistance programs to their platform and they didn't stop there! Extensive filters that allow for selection of specific client needs such as type (ie. SFR, manufactured homes, condos, multi-family, ADU’s), uses like renovation, above AMI income levels, non-1st time homebuyers are just a few of the filters you will find along with stand alone 2nd mortgages, combined 1st and 2nd mortgages and grants. DownpaymentResource.com is also in many MLS systems across the US and provides limited directory information and a free landing page for realtors to promote that they use DPA. Both MLO’s and realtors can subscribe to Down Payment Connect to get more of the extensive directory and back-end tools. Now, through HomePrep, HUD counselors can also use the Down Payment Connect system to filter trhough DPA programs that clients are qualified for, and can even provide wholesale programs when working with an independent loan originator (often called a mortgage broker)! Through HomePrep, HUD counselors are now able to provide MLO’s and clients with the DPA programs that they have found the client is eligible for.

Clients2Homeowners.com makes a pivot!