Equal Housing Lender

A Simple, Targeted Program Can Grow Your Future Mortgage Business

Contributors • March 11, 2020

In 1990, five years into my career in the mortgage business, I learned something from a successful new construction salesman that stuck with me for the last 30 years. The salesman’s name was Ed and he was the highest producing salesperson for a major builder. What was Ed’s secret? He listened to every prospect that came to his model center. If they weren’t ready to purchase a home yet, Ed would find out why and discuss the timeframe before they could purchase. After the prospect left, Ed would write conversation details on a card and file it in a small box that was always with him. It was not uncommon to see Ed pull out the “ready clients” to follow up with. It was also common for the builder to get notes that praised Ed’s follow-up as the reason that the prospect finally purchased a home! Ed simply determined an approximate time a client would be ready to purchase and then faithfully followed up to get their business.

From 2016 through 2019, I was on a U.S. Department of Housing & Urban Development (HUD) committee called the “ Housing Counseling Federal Advisory Committee (HCFAC) ”. While serving, I learned a great deal about what HUD-approved housing counselors could do to get clients ready for a home purchase. Housing counselors can help clients to correct, build and consolidate credit. Many counselors know about downpayment assistance programs, often more than my mortgage colleagues. And housing counselors educate clients on the proper budgeting needed to own a home. They are aware of the reasons that keep clients from purchasing a home … but work with these clients to get them ready for homeownership.

How many of us try ourselves to assist challenged clients … until business picks up and needed attention becomes scarce? What if there was a valid resource to send these clients to for detailed help to get “mortgage ready?” That resource is a HUD-approved housing counselor.

So I and others on the HUD HCFAC worked with housing counselors to develop a simple, structured path for loan originators to refer challenged clients to HUD-approved housing counselors. Similar issues that prevent a home purchase were narrowed to three specific areas of greatest need:

► Credit: Whether negative credit, no credit or too much debt (and NOT credit repair!)

► Downpayment assistance: Including wholesaler programs available to independent mortgage professionals!

► Budgeting: Saving for a home purchase

►

Student Loan Debt Relief added

Utilizing housing counseling agencies (HCAs) is already done by banks who consistently send challenged clients to HCAs and pay for services with Community Reinvestment Act (CRA) funds. But independent mortgage loan originators don’t have CRA funds to pay for services and most are not even aware of what housing counselors can do to assist clients.

To make this path possible, a memorandum of understanding (MOU) was created to serve as an agreement between the challenged client and the loan originator and is provided to the HUD housing counseling agency. The MOU states that the (pre-determined) cost for housing counseling services paid upfront by the client will be credited back towards closing costs on a future mortgage by the referring loan originator (the MOU can also be used with real estate agents). The MOU outlines services and credit to be provided and was developed with direction from the HUD Model Funding Agreements and Fee Structures Manual.

This provides multiple benefits to mortgage loan originators. The structure allows for:

►An MOU for credit towards closing costs on a future mortgage from the referring loan originator if the client returns to that originator for their mortgage.

►A bank loan originator who already uses housing counseling services that are paid for by CRA funds from their institution to continue using housing counseling services with the MOU agreement for credit if they migrate to the independent loan originator side of business.

►A partnership with a HUD housing counselor who is trained to take care of client issues and will notify the loan originator when the client is “mortgage ready.”

►Continued communication between a loan originator and a real estate agent about a referred client who is getting “mortgage ready.”

►Never saying “no” to a client! Provide the option for help with a HUD housing counselor.Consistent communication between the loan originator and the HUD housing counselor provides your “approximate date of follow-up” to update your “future client cards” in your own box. I know, because it’s working for me.

Stay tuned.

Pam Marron (NMLS#: 246438) is senior loan originator with Innovative Mortgage Services Inc. (NMLS#: 250769) in Tampa Bay, Fla. She may be reached by phone at (727) 375-8986, e-mail PMarron@InnovativeMortgage.onmicrosoft.com or visit CloseWithPam.com .

the number of down-payment assistance programs is on the rise, and a growing share are open to people of all income levels — even six-figure earners.

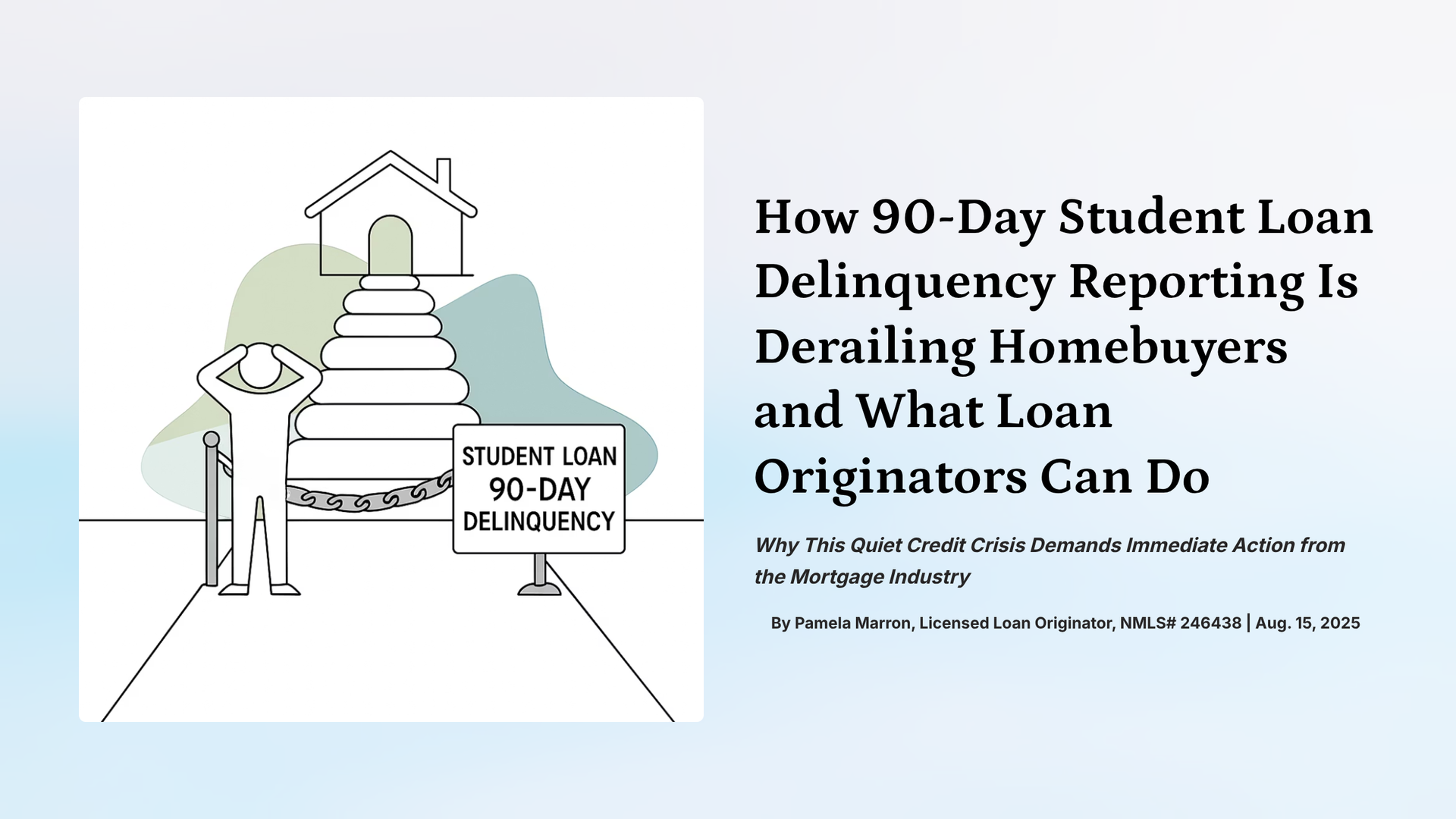

90-day student loan delinquencies are silently crushing credit scores and killing mortgage approvals. Here’s how MLOs can fight back.

A Few Extra Points MLOs Need to Know For Clients With Student Loans