Equal Housing Lender

Facing Negative Challenges Often Results in Unexpected Solutions

Contributors • September 26, 2019

The mortgage market is changing, and some negative challenges will occur. Many of us don’t talk with each other about problems because they may seem too complicated, perceived as negative, or out of fear of hurting our business. Instead, think through problems and collaborate with others on a solution, especially when you’ve been through the problem before. Confidence comes from getting in front of it.

For the past 10 years, my mortgage efforts have focused on assisting clients with issues that arose out of the housing crisis. Some of the problems were complex where proof was not visible and had to be dug for. Taking these problems to agencies and people who could help was usually met initially with negative skepticism until proof and research could be shown.

I have learned where to take my problems, but still face skepticism. Having a solution that can be built on is the best plan to get help. When others know that you’re not dropping an issue in their lap to totally solve and that their help is needed with a solution in progress where groundwork has already been done, the walls come down. Know the objections upfront and make sure potential corrections are presented.

For years, I have taken issues to the mortgage industry for their support to troubleshoot and advocate for solutions. But if the problem does not affect enough clients, or is misunderstood or perceived as negative, it is not taken up.

When I became a member of the HUD Housing Counseling Federal Advisory Committee (HCFAC), a 12-person group that consisted of folks from the mortgage, real estate and housing counseling industries as well as three consumers, it became evident that solving issues at the housing counseling level where clients can get the pre-purchase help first could be more productive.

So why did I think that mortgage professionals were the place to go to for help in the first place? I recalled faithfully attending “Bagels and Brokers” during the housing crisis, a monthly casual think-tank of a consortium of mortgage loan originators, wholesalers and mortgage affiliates who gathered and discussed mortgage issues and where to go for the solution. I came to realize that, though mortgage professionals may bring up a problem, their strength is in applying the correct solutions. Stepping back a few paces to see where to get a problem solved is necessary when your first option does not work.

A pilot program that connects housing counselors and loan originators to assist clients that need pre-purchase help was started in Tampa Bay, Fla. Successful client assistance is being experienced but news of what Tampa Bay CDC can do for clients has been slow to get out. After doing a presentation with Tampa Bay CDC at People Places LLC about what housing counselors could do to get clients “mortgage ready,” a successful business owner contacted me regarding how the pilot could assist his employees in gaining homeownership in the area. He told me success stories of how he and the employees benefited when they purchased homes and contributed to the local economy. Also, his brother owns a large real estate franchise in Tampa Bay and he wanted to know how the pilot program was different from the help already being provided to the real estate franchise for clients. I was able to tell him that the pilot concentrates on three areas: 1. Assisting clients with credit correction and credit building; 2. Assessing clients for all downpayment assistance available, including programs from mortgage wholesalers; and 3. Budgeting.

4. Student loan debt relief added. Prior to this call, I was targeting promotion towards mortgage professionals and real estate agents to begin the pilot. Now I am adding businesses.

There are times in the mortgage business where client needs become more prevalent than client desires. Client needs during a tighter market requires full attention to solutions and patience with moving parts. This is the time that mortgage loan originators need to have fine-tuned knowledge of mortgage products and know specific differences between Fannie Mae and Freddie Mac automated systems. Some loan originators may think of this as a negative because more attention needs to be paid to tedious detail to make a deal work. When times are good and property inventory is not as tight as it is right now, anyone can survive in the mortgage business. Count it as a positive when a real estate agent with a challenged client calls you, even if they referred the client to another loan originator first.

Stay tuned. Pam Marron (NMLS#: 246438) is senior loan originator with Innovative Mortgage Services Inc. (NMLS#: 250769) in Tampa Bay, Fla. She may be reached by phone at (727) 375-8986, e-mail PMarron@InnovativeMortgage.onmicrosoft.com or visit CloseWithPam.com .

the number of down-payment assistance programs is on the rise, and a growing share are open to people of all income levels — even six-figure earners.

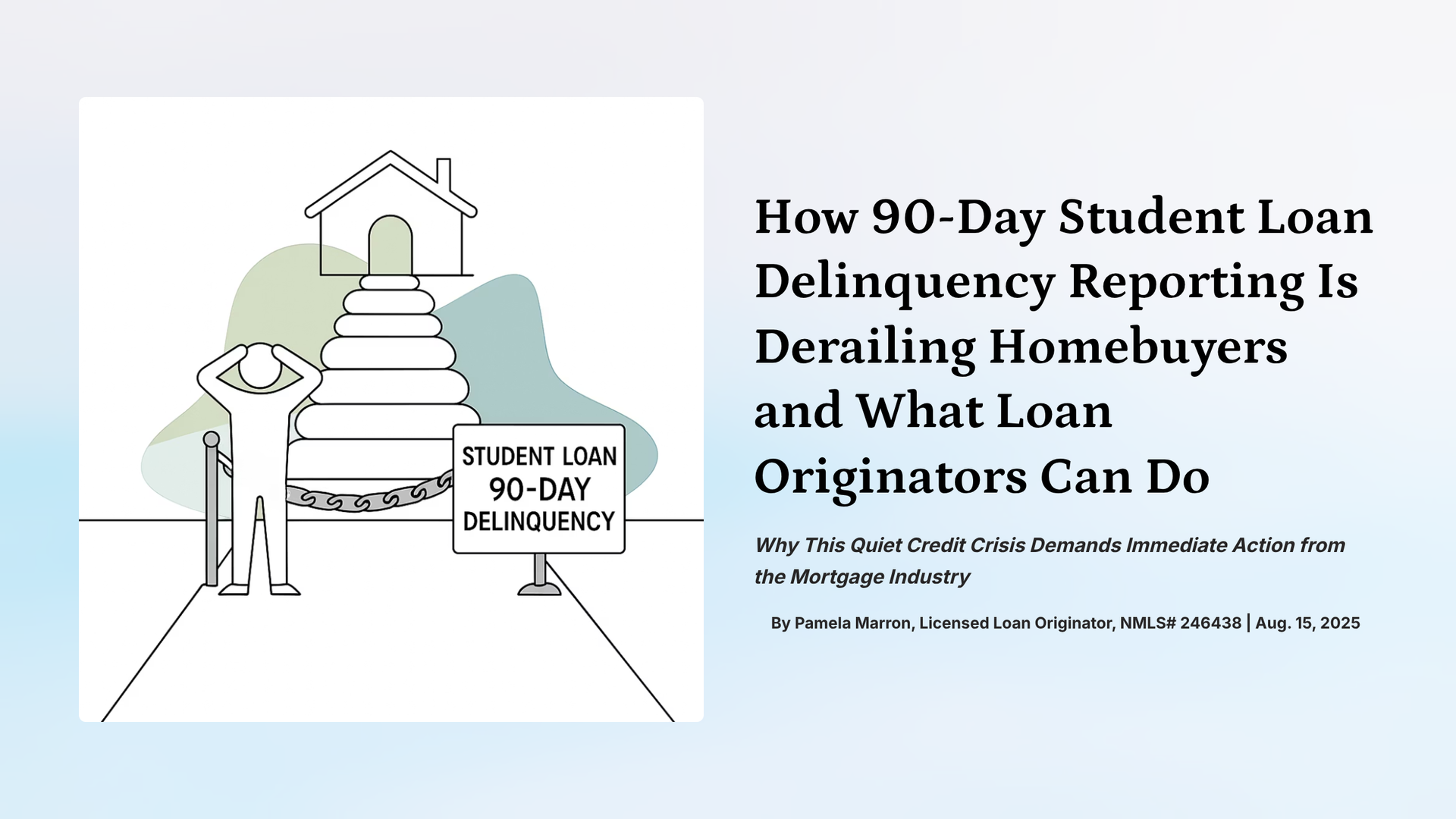

90-day student loan delinquencies are silently crushing credit scores and killing mortgage approvals. Here’s how MLOs can fight back.

A Few Extra Points MLOs Need to Know For Clients With Student Loans