Equal Housing Lender

A realization, facts, keeping watch on credit… and a new resource just in time

Contributors • May 28, 2020

By Pamela Marron | May 2020 | National Mortgage Professional Magazine

Realization

Clients NEED mortgages now, whether for a purchase or refinance. Even though uncertainty about COVID 19 looms, many are still cautiously purchasing homes or refinancing. Need is the driving force in spite of COVID 19. For purchasers, the need is a deadline date… that their lease is ending, or their existing home is closing, or their landlord is selling the home they rent. For those that refinance, cashing out on some of their existing equity for reserves or reducing payments for tighter budgets is the reason.

Know the facts

Know facts of mortgage options for those who may temporarily struggle to pay. You are going to need this information when you can provide these same clients with a mortgage as soon as they get back on their feet.

A massive number of job losses have occurred. Many homeowners are still employed but hours may have been drastically cut. Both Fannie Mae [1] and Freddie Mac [2] came out with a forbearance policy that allows a temporary suspension or reduction of mortgage payments and FHA provided similar policy with a partial claim option [3]. Initial talk speculated that the full amount of mortgage payments not made during the 60 to 90 day forbearance period would be due at the end of the forbearance timeframe and there are some references out there that support that thought. But both Fannie Mae [4] and Freddie Mac [5] as well as FHA have now stated publicly that per the Cares Act [6], there will not be a requirement to pay missed payments all at once unless you can.

Keeping watch on credit

Verbiage in the Cares Act states under HR748-(pg)209 (credit) (ii) REPORTING.- Except as provided in clause (iii), if a furnisher makes an accommodation with respect to 1 or more payments on a credit obligation or account of a consumer, and the consumer makes the payments or is not required to make 1 or more payments pursuant to the accommodation, the furnisher shall— ‘‘(I) report the credit obligation or account as current; [6]

Additionally, a forbearance approval letter from PennyMac obtained from a client states under Credit Reporting: “By entering into this forbearance plan, we will report your account to the credit bureaus as current under the forbearance plan.”

I asked Terry Clemans, director of the National Consumer Reporting Association (NCRAinc.org) how we could trust that delinquency during the forbearance period would be reported correctly. My concern was due to a credit issue during the housing crisis where foreclosure credit code showed up on past short sale credit when mortgage delinquencies were past 120 days. Though not the same issue, this code problem stalled or halted conventional financing for 3 additional years.

Mr. Clemans reminded me that there was no national emergency proclaimed during the housing crisis. A national emergency proclamation was issued effective March 1st, 2020 and prior to the forbearance directives. There is specific Metro 2 credit code for accounts affected by a natural or declared disaster. As long as loan servicers apply code correctly, borrower credit should not be negatively affected during publicly stated forbearance periods.

Those that can qualify to refinance on the other side of this pandemic will most likely NEED a refinance, and urgently. There will be changes as issues arise, but many of us are keeping a close watch on what credit looks like after the forbearance.

A new resource just in time

During my time on the HUD Housing Counseling Federal Advisory Committee (HCFAC) from 2016-2019, I learned a great deal about how much HUD housing counselors and certified credit counselors could do to help challenged clients – both pre-purchase and post-purchase.

That realization is what started a path to connect loan originators and realtors to housing and credit counselors to get challenged clients “mortgage ready”.

On May 28th, a webinar that shows loan originators and real estate agents how to make this connection and the benefits of doing so will be presented through the National Mortgage Professional Magazine. A website, www.Clients2Homeowners.com, was developed to house steps to connect and resources for credit help, downpayment assistance and budgeting for clients. Industry professionals will be on the call. Loan originators, real estate agents and housing counselors, this is open to all of you!

Remember to say “Thank You!” to invaluable frontline workers everywhere.

Stay tuned.

[1] Fannie Mae | Forbearance: https://www.knowyouroptions.com/options-to-stay-in-your-home/overview/forbearance [2] Freddie Mac Forbearance: http://www.freddiemac.com/about/covid-19.html [3] HUD Mortgagee Letter 2020-06 | April 1, 2020: https://www.hud.gov/sites/dfiles/OCHCO/documents/20-06hsngml.pdf [4] Fannie Mae | April 27, 2020: Understand Your COVID-19 Mortgage Options | Fannie Mae reminds homeowners they are not required to repay missed payments all at once: https://www.fanniemae.com/portal/media/corporate-news/2020/covid-19-mortgage-options-7010.html [5] Freddie Mac: Lump Sum Repayment is Not Required in Forbearance | April 27, 2020: https://freddiemac.gcs-web.com/news-releases/news-release-details/freddie-mac-lump-sum-repayment-not-required-forbearance?_ga=2.141393010.1330337281.1588780547-2108693110.1588422977 [6] Coronavirus Aid, Relief, and Economic Security Act (CARES Act): https://www.congress.gov/116/bills/hr748/BILLS-116hr748enr.pdf

the number of down-payment assistance programs is on the rise, and a growing share are open to people of all income levels — even six-figure earners.

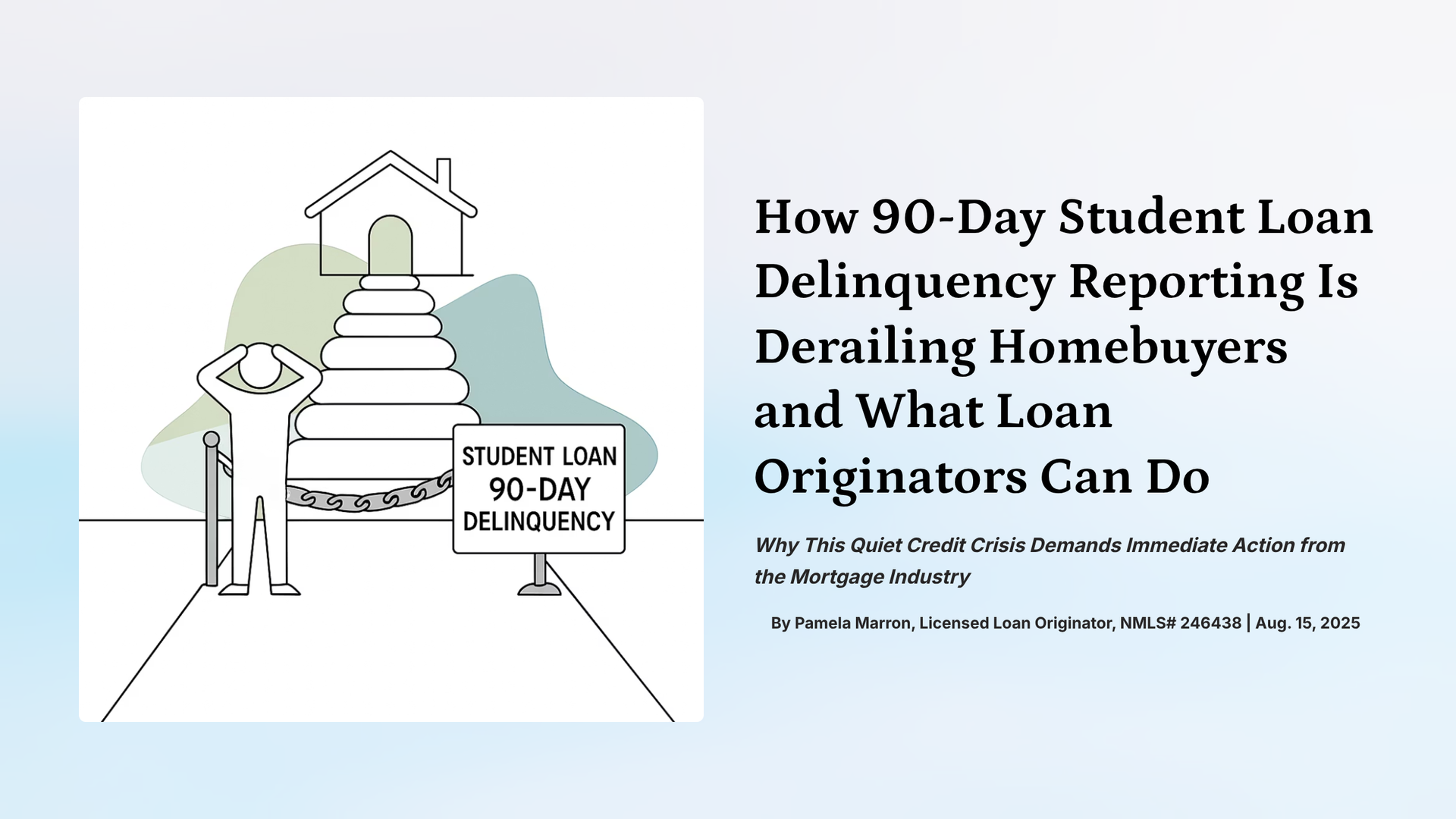

90-day student loan delinquencies are silently crushing credit scores and killing mortgage approvals. Here’s how MLOs can fight back.

A Few Extra Points MLOs Need to Know For Clients With Student Loans