Equal Housing Lender

Education Series for Most Needed Services to Assist Clients Trying to Get “Mortgage Ready”

By Pamela Marron, Loan Originator, NMLS#246438 • December 9, 2022

Focusing on Specific Client Needs, What Tools Can Be Used to Assist, and How to Bundle Targeted Services to Reduce Costs

A Pilot program called Home Prep that connects mortgage loan originators (MLO) to HUD housing and credit counselors who can get clients past final hurdles to become “mortgage ready” has been finetuning details on the areas where prospective mortgagors need the most help. Presently, the area of most need is for short and long-term credit help, though down payment assistance is a very close second place. It has been found that MLO’s and HUD counselors often work with the same resources but utilize these resources differently.

Discussion and awareness of WHY, WHAT, and WHEN to use specific resources has become a learning curve for both sides and has also provided surprises like bundled, targeted services that can save MLO’s and HUD counselors money as they get clients “mortgage ready”.

Series articles will focus on known issues, available tools that mortgage professionals and HUD housing and credit counselors can use with clients, along with guidelines and visuals to implement.

1st Series Article: Getting a Client “Mortgage Ready” by Working on the Best Possible CREDIT Before Starting Anything Else Is the 1st Step.

Everything BETTER for a mortgage starts with the BEST, MOST ACCURATE CREDIT possible. The BEST CREDIT leads to better interest rates, the lowest down payment required, access to best and most down payment programs that client may be eligible for, and automated underwriting approval when required.

Credit Issue: Deleting Disputes

Dealing with disputes is a common issue that can show up in Fannie Mae and Freddie Mac automated underwriting system (AUS) findings.

Credit repair companies often dispute accounts to improve credit scores. Sometimes those same disputes must be removed from the credit report to receive a Fannie Mae and Freddie Mac automated underwriting system (AUS) approval. Why? Because disputes hide credit. When the dispute is removed, negative credit may return.

1. What Dispute notification in Fannie Mae Desktop Originator/Underwriter Findings looks like

2. Fannie Mae Selling Guide Directions to follow for deletion of noted

Disputed Credit Report Tradelines

The entirety of direction to follow in the Fannie Mae Selling Guide for disputes on a credit report is below.

When the credit report contains tradelines disputed by the borrower, DU will first assess the risk of the loan casefile using all tradelines, including those disputed. If DU issues an Approve recommendation using the disputed tradelines, no further documentation or action is necessary. DU will issue a message specific to this scenario.

If DU does not issue an Approve recommendation when including the disputed tradelines, DU will re-assess the risk without using the disputed tradelines. If DU is then able to issue an Approve recommendation, the lender must investigate the tradelines to determine whether the borrower is responsible for the accounts or if the account information is accurate or complete.

- If the borrower is not responsible for the disputed accounts, the lender must obtain supporting documentation and may deliver the loan as a DU loan. No further action is necessary regarding the disputed tradelines.

- If the borrower is responsible for the disputed account, the lender must investigate the information, including determining the aspect of the tradeline that is being disputed. If the borrower is able to provide documentation to disprove any adverse information (such as canceled checks), the lender may deliver the loan as a DU loan.

- If the borrower is responsible for the disputed account and the account and tradeline information is accurate and complete, the loan is not eligible for delivery as a DU loan. The lender may manually underwrite the loan if the transaction is eligible for manual underwriting.

- A borrower’s account was referred for collection by the creditor. Subsequently, the borrower paid off the account, but the pay-off was not reported on the tradeline. The borrower requested that a dispute be placed on the tradeline. The tradeline information was accurate, but because it did not reflect that the borrower paid off the account, it may be considered incomplete. The borrower must provide documentation that the account was paid in full.

- A borrower and his son have the same name (Sr. and Jr.). The borrower’s credit report contains a tradeline that actually belongs to the son. The tradeline is reported as disputed. The borrower can provide confirmation that he is not obligated on the account.

- The servicer of a disputed loan indicates a late payment in January of the previous year. The borrower can provide documentation (such as canceled checks or bank statements) that indicate that the payment was made on time.

- The credit report indicates a disputed tradeline on the borrower’s mortgage being refinanced. The tradeline indicates a 60–day late payment in January of the previous year. The borrower cannot provide any documentation to support that the payment was made on time.

The monthly payments for the disputed tradelines must be included in the debt-to-income ratio if the accounts belong to the borrower.

Note: Tradelines reported as medical debt are not shown in the disputed tradeline message. Therefore, lenders are not required to investigate disputed medical tradelines.

Examples

The following scenarios are examples of when a loan receiving an Approve/Eligible recommendation with the disputed tradeline(s) excluded from DU's risk assessment would be eligible for delivery as a DU loan:

The following scenario is an example of when a loan receiving an Approve/Eligible recommendation with the disputed tradeline(s) excluded from DU’s risk assessment would not be eligible for delivery as a DU loan:

3. How to use

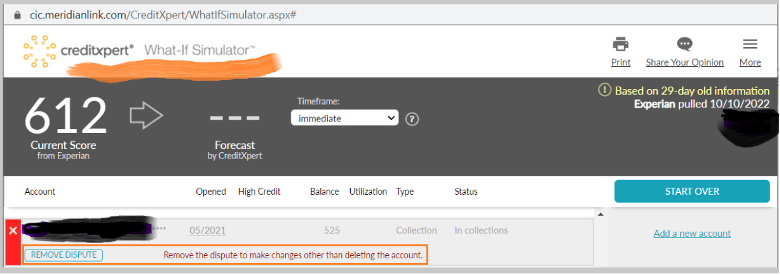

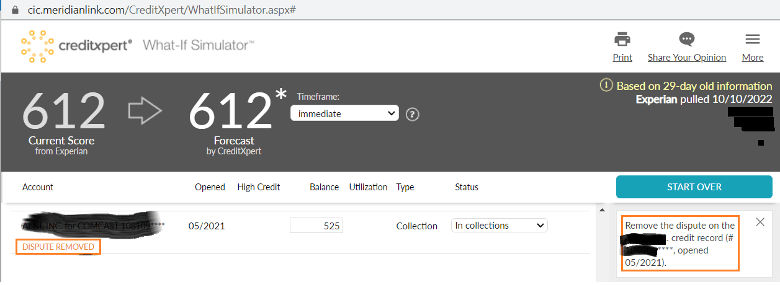

CreditXpert What-If Simulator to check what credit score will be when dispute is removed

Go to time 3:30 on CreditXpert What-If Simulator video[1] to find out how the removal of a dispute will affect your clients credit score.

How to check: Click on “REMOVE DISPUTE” button on CreditXpert What-If Simulator

IMPORTANT: Removing a Dispute does not always change the credit score.

- Directions for the client are listed on the right.

- The CreditXpert timeframe for what a client can do to change the score are only available to you for 30 days from the date the credit report is pulled.

You can check 1 or all 3 bureaus (Experian, Equifax, TransUnion) for a credit score change when deleting a dispute. Additionally, check with your credit reporting agency and ask for bundled costs for both soft and hard pull credit reports with the CreditXpert tools added to ALL credit reports. You may find that the cost per credit report may be more, but the monthly credit report bill, especially using soft pulls, to have CreditXpert on ALL credit reports rather than paying individual CreditXpert costs is less. (I am using CreditXpert that much!)

Next: 2 more credit tools: Wayfinder. Then, Meridian Link. Stay tuned.

[1] CreditXpert What-If Simulator Directions on YouTube for Dispute AND MORE at 3:30: https://creditxpert.com/credit-insights/xpert-tip-creditxpert-what-if-simulator-all-the-actions-you-can-simulate/

Writer Pamela Marron is a licensed Loan Originator NMLS #246438 in Florida who works for Innovative Mortgage Services, NMLS #250769 in Lutz, Fl. Articles written are strictly her opinion and are published to help loan originators, real estate professionals and mortgage clients. This is not used to solicit for business.

Pam Marron | NMLS# 246438

Tara Jerse | NMLS# 2105127

Innovative Mortgage Services, Inc. | NMLS# 250769

Equal Housing Lender

the number of down-payment assistance programs is on the rise, and a growing share are open to people of all income levels — even six-figure earners.

90-day student loan delinquencies are silently crushing credit scores and killing mortgage approvals. Here’s how MLOs can fight back.

A Few Extra Points MLOs Need to Know For Clients With Student Loans